Consumer bankruptcy is an increasingly popular way to get rid of debts. The premise of consumer bankruptcy is to write off debts and start life anew. A definite advantage is that the Receiver becomes a party to court and bailiff proceedings against the Bankrupt. This means that creditors or debt collectors cannot effectively demand repayment of debts from the Fallen Person.

Consumer bankruptcy application

A consumer bankruptcy application is filed through the National Debt Register on an electronic form. This means that submitting such an application on paper, will involve having to resubmit it through a special system.

In a consumer bankruptcy petition, we indicate basic data such as name, surname, PESEL or place of residence. We provide an up-to-date list of our assets, debts to other entities or indicate whether anyone is indebted to us. Additionally, we indicate information about our income, costs of living and whether we have made any legal transactions in the last twelve months before the date of filing the petition, e.g. sale of a car exceeding PLN 10 000, flat or other rights. At the very end of the consumer bankruptcy petition, you should attach scans of documents from which the debt arises. We recommend using the assistance of a professional law firm, because in this way we may avoid the call to supplement formal deficiencies, if we forget to attach the necessary documents. If the bankrupt cares about time, it may delay the examination of the application for several months.

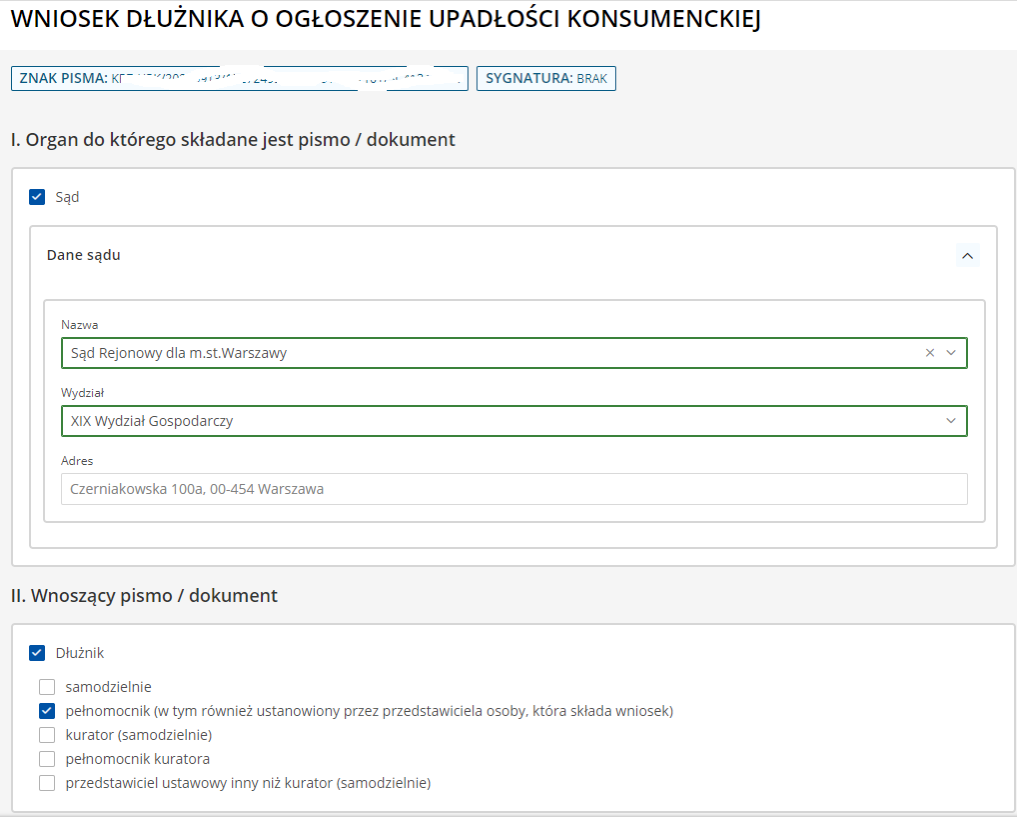

This is what the beginning of a completed consumer bankruptcy application looks like:

How much does consumer bankruptcy cost

Questions about the costs of consumer bankruptcy are very often asked before filing. The court fee on the bankruptcy petition is currently PLN 30. The remaining cost is the fee of the Law Firm that will prepare the consumer bankruptcy petition and represent the bankrupt after bankruptcy before the trustee. In less complex cases, the Law Firm’s fee is usually lower than in complex cases.

Would you like a quote for drawing up a consumer bankruptcy petition or for comprehensively handling the entire proceedings? Please contact us at [email protected]

Consumer bankruptcy how long does it take

The legislation does not set rigid time limits for consumer bankruptcy. It takes an average of 2-4 months to process a consumer bankruptcy petition, with up to 6 months in larger cities. The duration of consumer bankruptcy also depends on whether you cooperate with the trustee. Once a consumer bankruptcy is declared, he or she determines the composition and value of the bankruptcy estate and then sells the bankrupt’s assets and distributes the proceeds to creditors. If the bankrupt has no assets, such bankruptcy proceedings should last up to about six months. A plan for the repayment of creditors and the execution of the repayment of creditors is then established. This period depends on how long it takes the court to process the application. The creditors’ repayment plan is executed for a maximum of 3 years and its execution ends with the write-off of the bankrupt’s liabilities.

Consumer bankruptcy order:

Consumer bankruptcy and alimony

Consumer bankruptcy does not cover maintenance debts. This means that maintenance debts are not discharged, whether current or past due.

Outstanding alimony must be declared by the entitled person to the trustee on a special form. The trustee in bankruptcy places such a claim on the list of claims. This is an opportunity for them, as there is a good chance of recovering some of the overdue maintenance. Such maintenance creditors are satisfied first.

Once a consumer bankruptcy is declared, current maintenance payments are paid by the trustee. They enjoy priority of satisfaction over other debts. However, whether they are paid depends on whether the bankrupt had assets. If he or she is working and receiving a salary, they will be paid from his or her salary.

The Ministry of Justice has prepared a guide for those planning to file for consumer bankruptcy. It will certainly allow you to assess whether it is worth it.

Consumer bankruptcy and marriage

Consumer bankruptcy also affects the property regime of the spouses. Once bankruptcy is declared, a property regime of separation of property is created between the spouses. This means that if, prior to the filing of a consumer bankruptcy petition, the spouses had joint assets, these will be included in the estate. Generally, anything acquired during the marriage from joint funds is deemed to be joint property.

For this reason, spouses establish a property separation (prenup) in the expectation that they will retain their assets. It is only effective if it was concluded at least two years before the filing of the bankruptcy petition.

Example:

The couple established a property separation (prenup) on 8 August 2019. One spouse filed for consumer bankruptcy on 10 August 2022. In this case, more than 3 years have passed, so the spouses’ joint property will not enter the bankruptcy estate.

Consumer bankruptcy and mortgages

High loan instalments can lead to a loss of liquidity and, in the worst case scenario, to termination of the contract by the bank. If you have bought a dwelling in the past thanks to bank financing, it will be placed in a bankruptcy estate. This means that such a dwelling will be sold by the trustee and then the funds obtained from the sale will be transferred to the bank to pay off the mortgage. The surplus will be divided among the other creditors.

The situation will be more complicated if the dwelling is a joint asset of the spouses and the mortgage is taken out jointly. Also in this situation, the property will be sold, but the trustee will allocate an amount to the spouses that will allow them to rent the property for a period of 12 to 24 months.

Have you seen the latest blog posts?

Consumer bankruptcy and employment remuneration

As soon as bankruptcy is declared, the salary received becomes part of the bankruptcy estate. This means that remuneration for work is, in principle, subject to attachment by the trustee. However, the seizure may not exceed the amount corresponding to the minimum wage. In 2022, this is the amount of PLN 3010.00 gross. The trustee may seize up to 60% of the remuneration for work if the bankrupt is obliged to pay maintenance.

The receiver will most often send a letter to the employer indicating the amount of remuneration to be transferred by the employer to the receiver’s account.

We help you get through consumer bankruptcy! Write to us: [email protected]